Top navigation skipped

Glenn Hegar

Texas Comptroller

Korry Castillo, PTAD Director

Property Tax Today

Quarterly Property Tax News

Volume 6 | October 1, 2018

Property Tax Today features content regarding upcoming deadlines, action items and information releases.

Please let us know what you would like to see in future editions by sending property tax questions and/or suggested topics to ptad.today@cpa.texas.gov. We will gladly address property tax matters under our authority.

Message from the Comptroller

Glenn Hegar

Texas Comptroller

In July, I revised the Certification Revenue Estimate (CRE) to reflect better than expected revenue growth in fiscal 2018 and an improved economic outlook for fiscal 2019. Among other things, Texas has benefitted from rising oil prices and production, a subsequent increase in economic activity, over 350,000 new jobs in the 12 months ending in May 2018 and near historic lows in the state's unemployment.

As usual, the Property Tax Assistance Division (PTAD) kept busy this summer. In July, a group of PTAD staff came together with members of the Tax Assessor-Collectors Association of Texas to gain a better perspective on how the truth-in-taxation process functions in various counties across Texas. On Aug. 15, the 2017 Property Value Study (PVS) final results were certified to the commissioner of education. On Sept. 1, 2018, Korry Castillo took over as PTAD Director, replacing Mike Esparza, who retired after 30+ years in state government.

As we leave the heat of summer behind and head toward the holidays, PTAD has already begun working with legislators and their offices in preparation for the upcoming legislative session. It looks to be another busy one for property tax. Remember to attend the Property Tax Institute (PTI) in Austin, Dec. 4-5, to stay current on property tax matters in Texas.

Korry Castillo, PTAD Director

Hello from the (new) PTAD Director!

Since I joined the Property Tax Assistance Division on June 1, I focused my efforts on understanding our responsibilities, getting to know the team and meeting external stakeholders. In my new role as director of Property Tax Assistance, I will continue to work with the team to review division processes and prepare for the next legislative session.

I am so grateful for the wonderful PTAD team and the property tax professionals who have already supported me in this transition. I look forward to working with everyone in the Legislature, appraisal districts, tax offices and related industries in 2019.

Notes from the Field

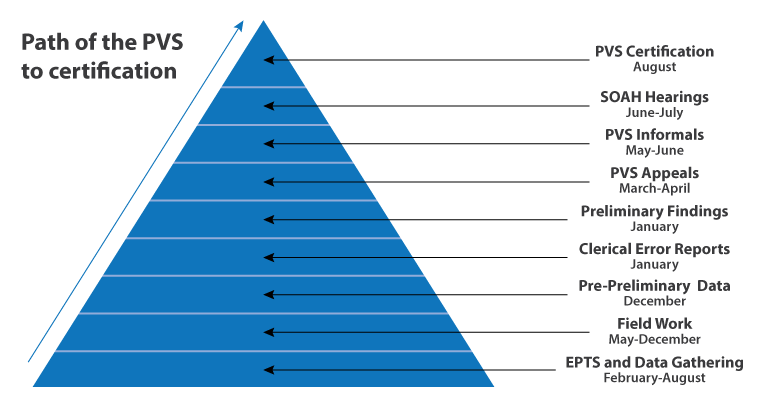

We often get questions about how we come up with the values for certification. As you can see in the related graphic, it is a long process. In preparation for the 2018 PVS, we received the first transfer of sales data and began gathering property information data in February. We began appraisal activities and related fieldwork in May.

We will continue with these activities through December, when we send pre-preliminary data to the appraisal districts for review. Appraisal districts typically have about 10 days to respond with any clerical errors found in the data. After addressing relevant clerical errors, our office certifies the preliminary PVS findings to the commissioner of education.

School districts or eligible taxpayers have 40 days from the certification date to file a protest (appeal), typically in mid-March. Our office reviews and accepts or rejects the appeals through April. During May and June, we hold informal meetings with protesting parties to try to come to a simple resolution. The protesting party may opt to appeal to the State Office of Administrative Hearings for a formal hearing if an informal agreement is not reached. These hearings typically occur in June or July.

Finally, at the conclusion of all hearings and data revisions, our office certifies the final PVS results to the commissioner of education by Aug. 15. We will certify the final 2018 PVS results in August 2019.

2017 PVS Final Results

On Aug. 15, 2018, the Comptroller's office certified the total 2017 value of all taxable property in each school district to the commissioner of education as required by Government Code Chapter 403. The 2017 PVS final taxable value findings are available on PTAD's Property Value Study and Self Reports webpage.

The 2017 PVS final findings indicate that 824 of the school districts studied received local value, and only 33 received state value.

Methods and Assistance Program (MAP) Reviews

Our office released the preliminary 2018 MAP reports on Sept. 13, 2018. We issue preliminary reports based on preliminary data received, documentation reviewed and on-site interviews conducted by the MAP reviewer. PTAD may make changes to reports after the release of the preliminary reports based on newly received data, documentation or other information. Appraisal districts must submit all remaining data for their final 2018 MAP reports by Nov. 1, 2018.

Appraisal districts scheduled for 2019 MAP reviews will receive a preliminary data request list in early November with a mid-December due date. A MAP team member will review all other information in the appraisal district offices.

Oil and Gas Operations on Ag Land

The Texas legislature passed a law, effective Sept. 1, 2017, that mandates open-space land's eligibility for special appraisal does not necessarily end because a lessee under an oil and gas lease begins conducting oil and gas operations (over which the Railroad Commission has jurisdiction). If the portion of the land on which the oil and gas operations are not conducted continues to qualify for appraisal, the eligibility remains. This does not, however, affect rollback tax from a change of use that occurred before Sept. 1, 2017.

PTAD is working with the Railroad Commission to provide examples of oil and gas operations that fall under the Railroad Commission's jurisdiction in the next update to the Comptroller's Manual for the Appraisal of Agricultural Land. Stay tuned!

Reinvestment Zone, Abatement and TIRZ

The Comptroller’s Data Analysis and Transparency (DAT) division encourages local governments, school districts and appraisal districts to submit the required reinvestment zone, abatement or tax increment reinvestment zone (TIRZ) forms, required by Tax Code Chapters 311 and 312, using our recently updated online forms. Appraisal districts with school districts that have created reinvestment zones for the purpose of executing Tax Code Chapter 313 agreements should complete Form 50-275. Forms are not required in areas that do not have reinvestment zones, abatements or TIRZ.

The Comptroller’s office is statutorily required to compile all reinvestment zone, abatement and TIRZ information received from local governments into a biennial report and submit such information to the Legislature prior to each legislative session.

Our March 2018 Tax Abatement Log (sortable and searchable) includes all reinvestment zone and abatement forms received by our office. Our 2016 Biennial Report (pgs. 34-51, 52-77 and 80-194) list TIRZ forms submitted to our office. Our 2018 report will be released in December. If you do not find your forms in either of these places, complete the appropriate forms and forward them to frank.alvarez@cpa.texas.gov or by mail as indicated in the form instructions.

For more information, see our FAQs and brochures for the Chapter 311 and Chapter 312 programs or watch one of our live webinars in November and December.

Appraisal Review Board (ARB) Surveys, Comments and Suggestions

The Comptroller's office is preparing the annual report summarizing property owners' comments and suggestions about ARBs received through our survey. Because surveys can only be submitted electronically, information from any handwritten surveys completed at the appraisal district office must be entered into the electronic survey no later than Dec. 1, 2018.

Additionally, taxpayer liaison officers in counties with populations exceeding 120,000 (as defined by the 2010 U.S. Census) must submit to the Comptroller's office a list of verbatim comments and suggestions received from property owners, agents or chief appraisers about the model ARB hearing procedures or any other matter related to the fairness and efficiency of the ARB. Please submit comments and suggestions received pertaining to these matters only in the appropriate Excel spreadsheet template to Kara Kelly no later than Dec. 31, 2018.

Chief Appraiser Eligibility

All chief appraisers must notify the Comptroller's office in writing no later than Jan. 1 of each year as to whether they are eligible to be appointed or serve as chief appraiser. Tax Code Section 6.05(c) provides that to be eligible to serve as chief appraiser, a chief appraiser must either be a certified Registered Professional Appraiser (RPA) or have the appropriate professional designation (Member Appraisal Institute (MAI), Assessment Administration Specialist (AAS), Certified Assessment Evaluator (CAE) or Residential Evaluation Specialist (RES)). A chief appraiser who is not an RPA but who has an MAI, AAS, CAE or RES designation must obtain an RPA certification within five years of his or her appointment or beginning of service as chief appraiser.

All chief appraisers must notify the Comptroller's office in writing no later than Jan. 1 of each year as to whether they are eligible to be appointed or serve as chief appraiser. Tax Code Section 6.05(c) provides that to be eligible to serve as chief appraiser, a chief appraiser must either be a certified Registered Professional Appraiser (RPA) or have the appropriate professional designation (Member Appraisal Institute (MAI), Assessment Administration Specialist (AAS), Certified Assessment Evaluator (CAE) or Residential Evaluation Specialist (RES)). A chief appraiser who is not an RPA but who has an MAI, AAS, CAE or RES designation must obtain an RPA certification within five years of his or her appointment or beginning of service as chief appraiser.

Chief appraisers must submit written notification using Comptroller Form 50-820, Tax Code Section 6.05(c) Notification of Eligibility or Ineligibility to be Appointed or Serve as Chief Appraiser. Please email completed forms to ptad.cpa@cpa.texas.gov .

Tax Bills

Taxing units usually mail their tax bills in October. Tax bills are due upon receipt, and the deadline to pay taxes usually is Jan. 31. Taxes become delinquent, and penalty and interest charges are added to the original amount beginning on Feb. 1. Failure to receive a tax bill does not affect the validity of the tax, penalty or interest due, the delinquency date, the existence of a tax lien or any procedure the taxing unit institutes to collect the tax.

You can find more information regarding payment of taxes, including deadlines, consequences for failure to pay and instances when a waiver of penalty or interest may apply, on PTAD's Paying Your Taxes webpage.

Payment Options

You can also find information regarding payment options on PTAD's Payment Options webpage. Tax collection offices are required to offer certain, but not all, payment options. Contact your local tax collection office to determine what local payment options may be available, such as:

- Credit card payment (Tax Code Section 31.06)

- Deferral (Tax Code Sections 33.06 and 33.065

- Discounts (Tax Code Section 31.05)

- Escrow agreement (Tax Code Section 31.072)

- Installment payment (Tax Code Sections 31.031 and 31.032)

- Split payment (Tax Code Section 31.03)

- Partial payment (Tax Code Section 31.07)

- Work contract (Tax Code Sections 31.035 – 31.037)

Operations Survey Data

Our office recently published the responses to the Appraisal District Operations Survey for the 2017 Tax Year on PTAD's Property Tax Survey Data and Reports webpage. See information below on the new visualization tool that presents Operations Survey data in the form of charts and graphs and allows for comparisons across multiple years and counties.

New Data Visualization Tools

PTAD recently published two new data visualization tools:

- The Tax Rates and Levies Data Visualization Tool allows users to explore and compare property tax rates and levies for counties, cities and school districts.

- The Operations Survey Data Visualization Tool allows users to explore data reported to the Comptroller's office by county appraisal districts regarding their budgets, staffing, appraisal services and operations.

Coming soon is an ARB data visualization tool that will allow users to explore data reported to the Comptroller's office about ARB members, protests, hearings and ARB operations.

Attorney General Opinion

The following opinion was issued by the Office of the Attorney General.

Opinion No. KP-0215 (Sept. 24, 2018)

Subsection 11.13(n) of the Tax Code provides that if a municipality adopts a tax exemption percentage that produces an exemption of less than $5,000 when applied to a particular residence homestead, the individual is entitled to an exemption of $5,000 of the appraised value. Because Article VIII, Section 1-b(e) of the Texas Constitution and the Legislature establish a legislatively-defined floor for the exemption in an amount of $5,000, a court would likely conclude that a home-rule municipality lacks authority to increase the floor above $5,000. Municipalities desiring to increase the homestead exemption must do so by raising the tax exemption percentage, up to 20 percent, as authorized in the Constitution.

The Legislature charged the chief appraiser with determining an individual's right to a property tax exemption, and the Commission of Licensing and Regulation prohibits appraisers from engaging in an official act that violates the law. If a taxing unit adopts an unlawful exemption, the appraiser maintains both a legal and ethical duty to determine that the exemption is inapplicable to the extent it violates the law.

Event News

Property Tax Assistance Division employees worked with members of the Tax Assessor-Collectors Association of Texas to strengthen their knowledge of the truth-in-taxation process in Texas and to build better working relationships between our office and local tax offices. There were a lot of great questions and discussion, and great working relationships were born. Attendees included:

Property Tax Assistance Division employees worked with members of the Tax Assessor-Collectors Association of Texas to strengthen their knowledge of the truth-in-taxation process in Texas and to build better working relationships between our office and local tax offices. There were a lot of great questions and discussion, and great working relationships were born. Attendees included:

- Bee County Assessor-Collector Linda Bridge;

- Comal County Assessor-Collector Cathy Talcott and her staff, Sharon Carlson and Monica Goodall;

- Denton County Assessor-Collector Michelle French and her staff, Stacy Dvoracek;

- Grayson County Assessor-Collector Bruce Stidham;

- Montgomery County Assessor-Collector Tammy McRae;

- Williamson County Assessor-Collector Larry Gaddes and his staff, Jeanette Guzmon, Rebecca Turner and Jen Wootton;

- Texas Association of Counties, Tim Brown; and

- PTAD staff: Elizabeth Alvarado, Andrew Belcher, Catie Burleigh, Korry Castillo, Heather Hampton, Kara Kelly, Stephanie Mata, Shannon Murphy, Sheryl Perry, Stephanie Rose, Charlotte Thomas, Leslie Ward and Craig Williams.

Action Items

Below is a list of action items for the third quarter of 2018. You can find a full list of important property tax law deadlines for appraisal districts, taxing units and property owners on PTAD's website.

- Oct. 16 - Farm and Ranch Survey responses due

- Nov. 1 - Final MAP documents for 2018 reports due

- Dec. 1 - ARB survey comments due

- Dec. 31 - Taxpayer liaison officer comments received due

- Jan. 1 - Chief appraiser eligibility forms due

If one of the deadlines is on Saturday, Sunday or a legal or state holiday, the act is timely if performed on the next regular business day.

Please be advised that the information in this newsletter is current as of the date of its publication and is provided solely as an informational resource. The information provided neither constitutes nor serves as a substitute for legal advice. Questions regarding the meaning or interpretation of any information included or referenced herein should be directed to legal counsel and not to the Comptroller's staff.